What has happened to the economies of the Middle East over the last decade? The last ten years have been ones of unprecedented drama because of the Arab Spring, its collapse and descent into war, and repression in most of the countries in which it occurred. This has obscured some very worrying underlying trends which were among the reasons why the Arab Spring occurred.

The first is demographic pressure (See Table 1). The population of the Middle East has increased by nearly over 100 million, or 22 percent in the ten years preceding 2017. The population of the Arab states rose by 83 million or a quarter, while the three non-Arab states increased more slowly. Israel’s population rise was close to the Middle East average. Egypt, the largest Arab state in demographic terms, experienced a rise of 20 million or nearly 26 percent.

These increases, which were among the fastest in the world, placed huge strains on the economies of the region. They required more food supplies in a region that is chronically short of water, investments in the infrastructure, and fast economic growth to generate jobs.

The growth of the total population did not fully reflect the severity of the problem. Between 2005 and 2015, the population of the Middle East and North Africa (excluding Israel and Turkey) aged 15 to 24 years rose by 55 percent from 47 million to 73 million. This meant that the growth rate of young people at labor market entry age was more than twice as fast as that of the total population. As a result, there were 26 million more people entering the labor market in 2017 than in 2007.[1]

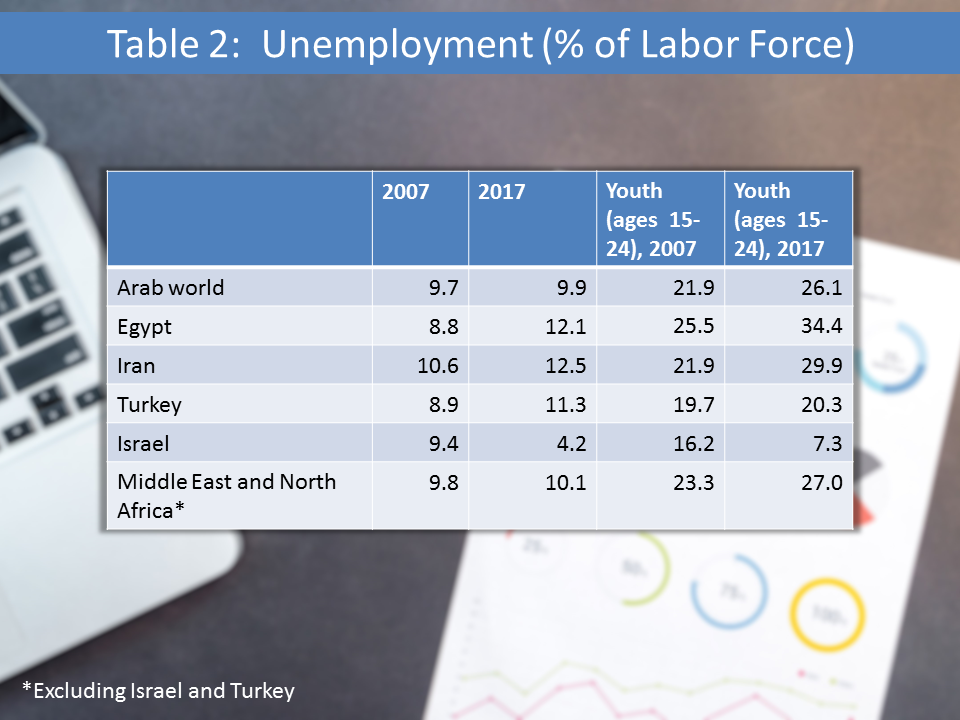

Given the weakness of economic growth, unemployment has increased, especially among youth (Table 2). In 2007, unemployment rates in Arab countries and Iran were among the highest in the world. By 2017, they had increased in those counties, as well as in Turkey. The rates of unemployment among young people were much higher. This was true in developed economies, such as Israel, but there the level of youth unemployment declined, as did the overall level of unemployment. In the Arab countries, Iran and Turkey, the rate of youth unemployment was even higher among females. In 2007, 45.6 percent of young females in Saudi Arabia were unemployed; in 2017 the figure was 46.3 percent. In Egypt there was an improvement, as the rate of unemployed young women fell went from 47.9 percent down to 38.5 percent largely because of growth of the informal sector. In Turkey the share of female youth unemployment in 2007 was 17.5 percent and in 2017 it was 25.6 percent, as total unemployment rose. In Israel the rate of unemployment among young women fell from 17.3 percent to 7.8 percent, as total unemployment fell.

The number of unemployed in much of the region has been understated. The low labor participation rate especially among females in Arab states meant that many did not enter the labor market. Much employment is partial, and yet part-time workers are not counted as unemployed. Furthermore, much employment was in the informal sector where earnings were low.

Unemployment rates are closely related to economic growth. Given a particular population growth rate, the economy needs to growth sufficiently to generate jobs for labor market entrants. If there is unemployment, then faster economic growth is needed. The problem is not only how to generate growth but how to do so in a way that creates jobs. The Arab countries have invested heavily in capital equipment (such as machinery and refineries) that is not employment intensive and this has been one of the factors behind chronically high unemployment rates.

Despite the damage inflicted throughout the region by war and large military spending, real national income has increased over the past ten years across the Middle East, as has income per capita (see Table 3). The large difference between these two growth rates reflects the effect of rapid demographic growth.

War has had enormous effects on economic developments in the region. In 2017, the World Bank has summarized them as follows. The war in Syria has killed about 500,000 people, displaced half the population (or over 10 million people) - one-third of them outside the country - and pushed more than two-third of Syrians into poverty. The refugees initially moved to Jordan, Lebanon, Turkey, and Iraq, and then reached Europe on a huge scale, causing an international displacement crisis.[2]

The conflict in Yemen has limited access to food, water, and health care, deepened poverty, and forced millions of children out of school. Thousands have been killed, and tens of thousands wounded. By 2017, more than 15 percent of the Yemeni population (over four million people) has been displaced or have fled the country. The war in Libya has displaced 10 percent of its six million population internally, and about 125,000 have fled the country, mainly to Europe.

These three civil wars have directly affected the lives of more than 60 million people, about one-fifth of the population of the MENA region. They have had effects on neighboring countries, which are hosting millions of refugees while their trade, tourism, and security were undermined. Furthermore, terrorist attacks, originating in the region, have spread around the globe.

In Syria, damage to the infrastructure by 2016 was estimated at between $33 billion and $42 billion. Between 2010 and 2016, output, measured in constant prices is estimated to have declined by two-thirds. Estimated foregone output (output if there were no conflict and the economy grew by 5 percent annually, on average) came to $200 billion or 300 percent of 2010 GDP. Moreover, the total costs of war in terms of economic output would nearly double if the losses due to the lack of trade integration within region were included.

Yemen has a long history of instability, but the conflict there has caused a massive humanitarian crisis. Economic activity has collapsed in most of the economy, particularly oil; access to social services, including health and education, has fallen sharply; and imports have declined substantially. Oil production, the main source of government revenue, fell sharply following the uprising in 2011 due to increased fighting in regions where the oil fields are located. An estimate of the damage to the Yemeni economy in the period 2011- 2015 was $15 billion. The fighting has since intensified, and so the damage has increased. In 2016, GDP was estimated at $11.9 billion compared to $30.9 billion in 2010, in constant 2010 prices. GDP per capita fell even more dramatically from $1,309 in 2010 to $431 in 2016. Since then, conditions have worsened even more.[3]

War, insecurity and violence have affected more than three million people or half the population in Libya. An estimated 2.4 million people are in need of protection and humanitarian assistance. These include about 241,000 internally displaced persons, about 437,000 non-displaced persons with special needs, and another 125,000 refugees fleeing to Europe and Italy in particular. Militia control of the main oil terminals of Ras, Lanuf, Sidra, Zueitina and Brega for almost three years has cost Libya over $100 billion in lost revenue. Real GDP is estimated to have declined by 8.9 percent in 2015 and it shrank further by 2.5 percent in 2016. Per capita income has fallen from almost $13,000 in 2012 to less than $5,000 in 2016. (3) The World Bank has estimated that Libya’s GDP fell from $77.8 billion in 2010 to $46.6 billion in 2017, in constant 2010 prices. Per capita income fell by over 40 percent from $12,548 to $7,281.[4]

According to the UN, the total number of people in the region forcibly displaced homes increased from 12.7 million in 2010 to 29 million in 2016. The number of international refugees originating from Arab countries rose from eight million to 13 million, and the number of internally displaced people from 4.7 million to 16 million. The number of refugees hosted by Arab countries rose from 7 million to almost 8.5 million; while the region has only 5.4 per cent of the world’s population, it has 37.5 percent of world refugees. The number of people in need of humanitarian assistance in Iraq, Libya, Somalia, the West Bank and Gaza, Sudan, Syrian Arab Republic and Yemen has risen. Some 56.4 million people required humanitarian help in 2016, with 37.2 million suffering food insecurity, 44.5 million in need of water, sanitation and hygiene assistance and 47.2 million health assistance. Of those in need, roughly half were women and nearly half children aged under 18 years of age. Countries in the region affected by conflict lost $614 billion cumulatively in GDP between 2010 and 2015, or six per cent of the regional GDP.[5]

Between 2007 and 2017, military spending in the Middle East and North Africa rose by almost 37 percent in real terms from $142 billion to $194 billion.[6] This meant that in 2017 about six percent of national income was spent on the military. A very approximate estimate suggests that in the decade in question the region spent about $1.7 trillion on defense. This calculation excludes Syria, whose military budget is not known. These huge sums could have been spent on civilian projects and represent the opportunity cost of the tensions and wars in the region. Imports of weapons into the Middle East and North Africa rose from $20.2 billion in 2007 to $41.2 billion in 2015.[7]

The region was also affected by dramatic changes in oil prices. They rose to a peak of just over $109/barrel in 2012 and then fell to $49.95 in 2015. The effects of these price fluctuations as well as changes in the volumes exported on the revenues of OPEC members in the Middle East are shown in Table 4. Between 2009 and 2012, oil revenues rose by 98 percent. Then, between 2012 and 2016, they declined by 61 percent. The changes in Iranian revenues were even more dramatic because of the effects of sanctions.

The Middle East is rich in oil but poor in water. It is the world's most water-scarce region and the situation is worsening due to the effect of conflict, climate change, and slow or even negative economic growth. The water crisis threatens the region’s stability as well as its human development and growth. Water resources per capita in the Middle East account for just one-sixth of the global average and they continue to fall. Every country in the region is experiencing groundwater depletion, with very high rates of withdrawal of both surface and groundwater. As agriculture, the largest consuming sector, is struggling to compete for water with industry and other sectors. In addition, the climate, which is largely arid to hyper-arid and highly variable, is changing, with drought becoming more frequent.

While the region has five percent of the world’s population, it only has only about one percent of global total renewable freshwater resources, water that is naturally available and replenished by the hydrological cycle. Freshwater availability has fallen by 75 percent since the 1950s and is forecast to fall by a further 40 percent by 2030. Between 2007 and 2014, the amount of fresh water per capita in the Arab World fell by 20 percent, in Iran by eight percent, in Turkey by 10 percent and in Israel by 12.5 percent.[8]

Drought was a major factor behind the war in Syria. Between 2006 and 2010, Syria suffered a severe draught. This affected food security and has pushed 2-3 million people into extreme poverty; 800,000 people had their livelihoods ruined, mainly in the northeast of the country, but also in Deraʿa province with a population of 300,000. Small-scale farmers were the worst affected; many were unable to grow enough food or earn enough money to feed their families. As a result, tens of thousands left the northeast and now inhabit informal settlements or camps close to Damascus. Water sources have also been permanently affected, with farmers compelled to use wells to draw on groundwater resources due to a lack of rainfall. The situation is exacerbated by the inefficient use of water, and groundwater resources in many parts of the country have been exhausted.[9]

Massive investments have been made in desalination both in the Gulf Arab countries (and in Israel). This has increased the supply of water but at a cost. The Gulf states are heading for a salt crisis: the more they desalinate, the more concentrated wastewater or brine, is pumped back into the sea; and as the Gulf becomes saltier, desalination becomes more expensive. The process is costly and energy intensive; it pumps seawater through special filters or boils it to remove the salts. The resulting brine can be nearly twice as salty as normal Gulf waters.

The Gulf has become more like a salt-water lake than a sea. It is shallow, only 35 meters deep on average, and is almost entirely enclosed. The few rivers that feed the Gulf have been dammed or diverted and the region’s hot and dry climate results in high rates of evaporation. The daily dose of around 70 million cubic meters of super-salty wastewater from dozens of desalination plants means that the water in the Gulf is 25% saltier than normal seawater that parts are becoming too salty to use.[10]

How did these trends affect human development? The Human Development Index (HDI) is a summary measure of average achievement in key dimensions of human development: a long and healthy life, being knowledgeable, and have a decent standard of living. The HDI is the geometric mean of normalized indices for each of the three dimensions.

The human development index for Arab countries deteriorated in 2007-2017. This was the result of the wars in the region. Three countries suffered most, and this was reflected in dramatic declines in human welfare. Syria's ranking fell from 107 in 2007 to 155 in 2017; Libya fell from 55 to 108, and Yemen fell from 140 to 178.[11] If and when the wars end, then the Middle Eastern regimes—whether new or old—will face the same problems as their predecessors, but with greater pressures. There will be more people, in greater need of help because of the effects of war. There will be more unemployed because economic growth had been inadequate. There will be less water because of pollution, desertification and urbanization. The prospects of an oil-led boom have receded as US shale oil production increases. This is not a promising scenario and the current socio-political unrest brewing in Sudan, as well as in Algeria, Iraq, Jordan, Lebanon, Libya and Morocco, has already been labelled “a Second Arab Spring.”[12]

[2] World Bank. MENA Economic Monitor. The Economics of Post-Conflict Reconstruction in MENA. 2017.

[3] World Bank. https://data.worldbank.org/country/yemen-rep2.

[4] World Bank Data. https://data.worldbank.org/country/libya-rep.

[5] UN Economic and Social Council for West Asia. Arab Governance Report III. Institutional Development in Post-conflict Settings 2018.

[6] Stockholm International Peace Research Institute. Military Expenditure Database.

[7] United States Department of State. World Military Expenditure and Arms Imports 2017.

[8] World Bank. Beyond Scarcity: Water Security in the Middle East and North Africa; World Bank Data.

[10] https://www.theguardian.com/global-development-professionals-network/2016/sep/29/peak-salt-is-the-desalination-dream-over-for-the-gulf-states

[11] UNDP. Human Development Report. 2009; Human Development Indices and Indicators 2018 Statistical Update.

[12] https://www.theguardian.com/world/2019/jan/26/sudan-egypt-corruption-arab-spring?)